El crecimiento económico es débil y el más lento post recesión en un siglo ¿Quién arregla esto?...

por La Carta de la Bolsa •Hace 8 años

•Hace 8 años

5.00

5.00Hablo con uno de mis gurús favoritos. "El crecimiento global es el más lento post recesión en un siglo. Salvo España, la mayoría de los países ofrecen cifras raquíticas. En Europa, preocupan los registros del eje franco-aleman, como verán más abajo. La economía española creció un 0,8% en el segundo trimestre, con lo que ya acumula cuatro trimestres consecutivos creciendo a este ritmo, gracias al consumo de los hogares y al repunte de la inversión, que mostraron aumentos trimestrales del 0,7% y del 1,3%, respectivamente, según la Contabilidad Nacional Trimestral publicada el jueves pasado por el Instituto Nacional de Estadística. Este crecimiento del PIB del 0,8% iguala a los registrados en los tres trimestres previos (tercer y cuarto trimestre de 2015 y primer trimestre de 2016) y es una décima superior a la estimación que realizó el INE a finales del mes pasado (0,7%). Y crece la inversión: la ralentización de la demanda de los hogares y la caída del consumo de las AAPP se vio compensada por el mejor comportamiento de la inversión y también por una evolución muy positiva del sector exterior. A pesar de los avisos de que algunas empresas estarían retrasando sus decisiones a la espera de la formación de Gobierno, lo cierto es que creció un 1,3% en el segundo trimestre, un punto más que el trimestre anterior. España va bien y tiene inercia, aunque como ha dicho Guindos, la inercia se puede cabar en cualquier momento..."

"¿Qué pasa en el resto delmundo? Lo más llamatiov es lo conocidoel viernes pasado: EEUU revisa a la baja el PIB del segundo trimestre: creció el 1,1% frente al 1,2% inicial. Aún así se mantiene la expectativa de una sibida de los tipos USA en diciembre..."

"¿Por qué el mundo no crece? Se van a cumplir tres años desde que el BIS dijera ¿Por qué persiste seis años tras el inicio de la Gran Recesión el crecimiento débil? (A estos seis años aludidos hay que sumar los casi tres transcurrios desde entonces). Algunas respuestas:

* Deficiencia secular de la demanda

* Desaceleración en la innovación

* Deterioro demográfico

* Incertidumbre en la gestión oficial

* Deterioro del escenario político

* Elevada deuda acumulada

* Insuficiente estímulo fiscal

* Excesiva regulación financiera

***

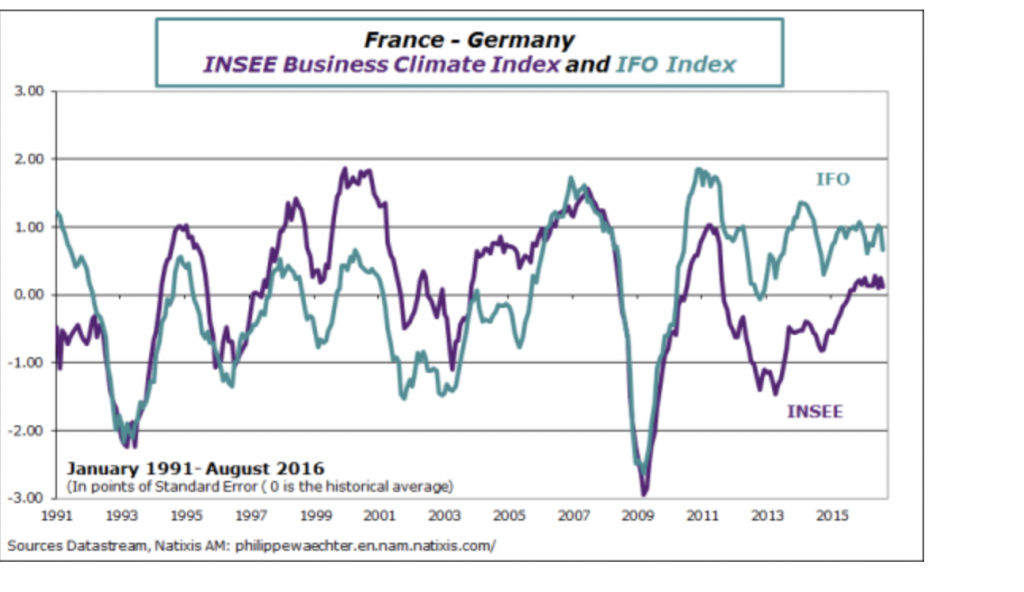

Y ahora el caso francés y alemán:

Germany and France on a slower momentum (Philippe WAECHTER, Chief Economist, Natixis AM)

According to companies’ survey in Germany and in France the economic activity was marginally down in August. German’s companies were a little more pessimistic for the 6 month period to come.

Even if levels are different we perceive in the following graph that there is a kind of stability in economic activity during the last twelve months. This synchronization of the business cycle suggest that France and Germany cannot really expect a stronger growth momentum in the short run. In other words, it seems that German and French economic activity are not able to accelerate from their current level. It’s not worrisome for Germany as its unemployment rate is low but it is problematic for France as its unemployment rate is just below 10%. As there is no impulse from outside as world trade trend is flat, it means that the impulse must come from inside. The ECB has done the job so we must expect a more proactive fiscal policy in order to jump on a higher trajectory.

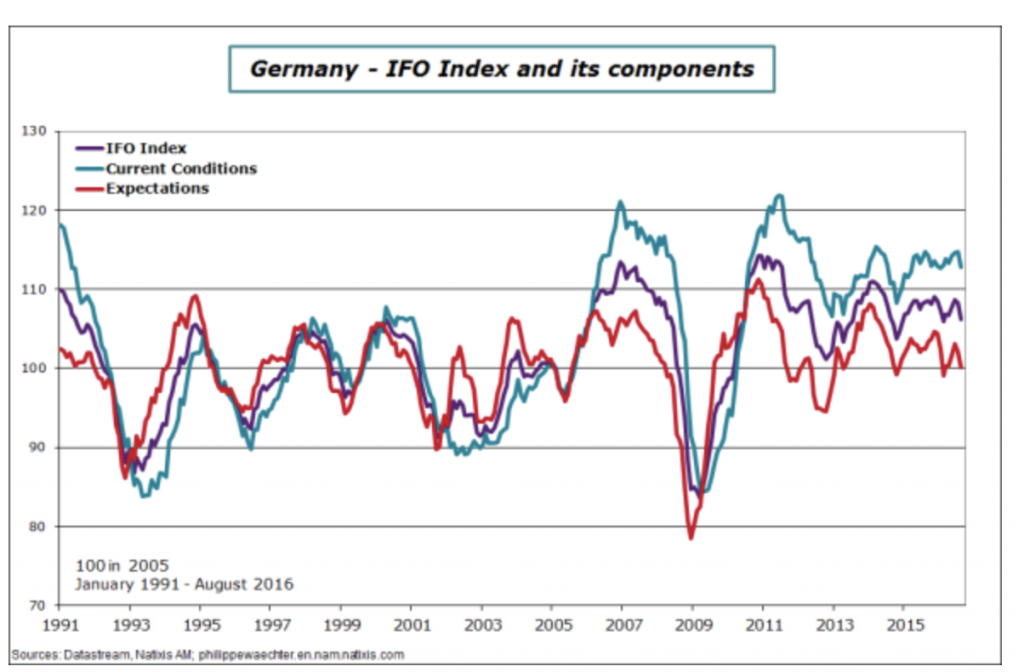

For Germany, the main source of weakness is a slowdown in expectations. The index is back to 100.1 which is marginally below its historical average (100.3). The current condition index (112.8) is weaker but at a level way above its historical average (103.2)

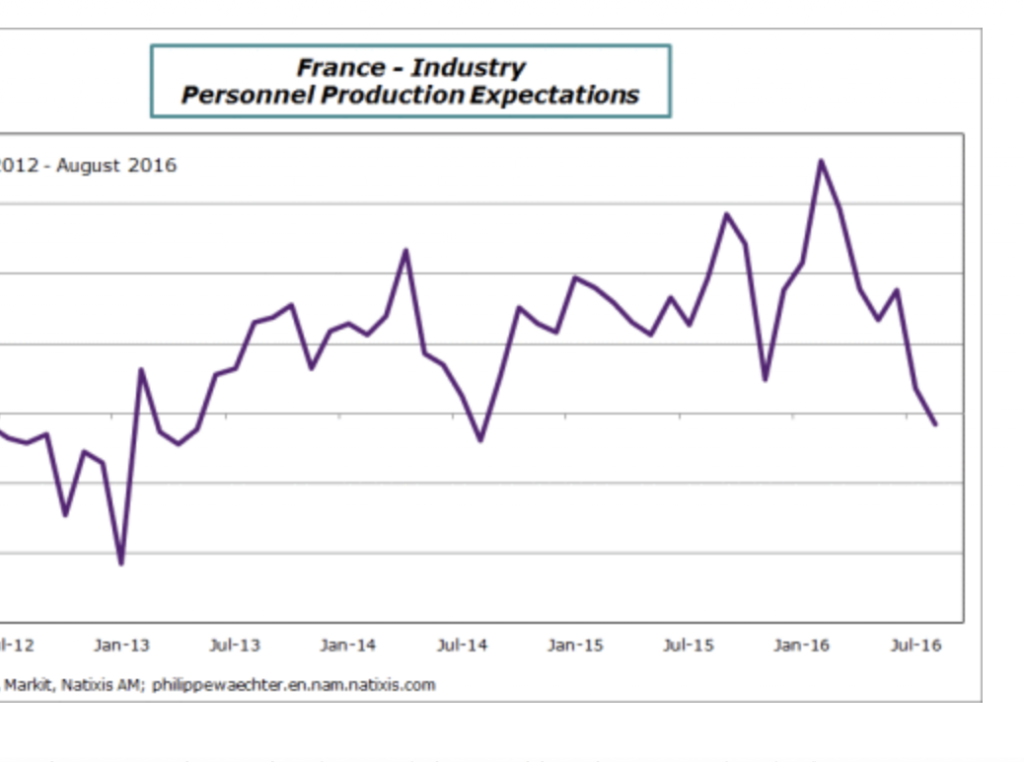

In France, the Personal Outlook index on Production is shifting downward in the industrial sector.

There is, both Germany and France, the perception by companies that the economic activity will not have the necessary impulses that could provoke an acceleration in the economic momentum. This can be linked with Brexit (see here) and its consequences or by the fact that the global situation is at risks and not only on economic side. We see political risks almost everywhere (elections in the US, in France, referendum in Italy, Brexit,…) and this could be a drag for economic growth.

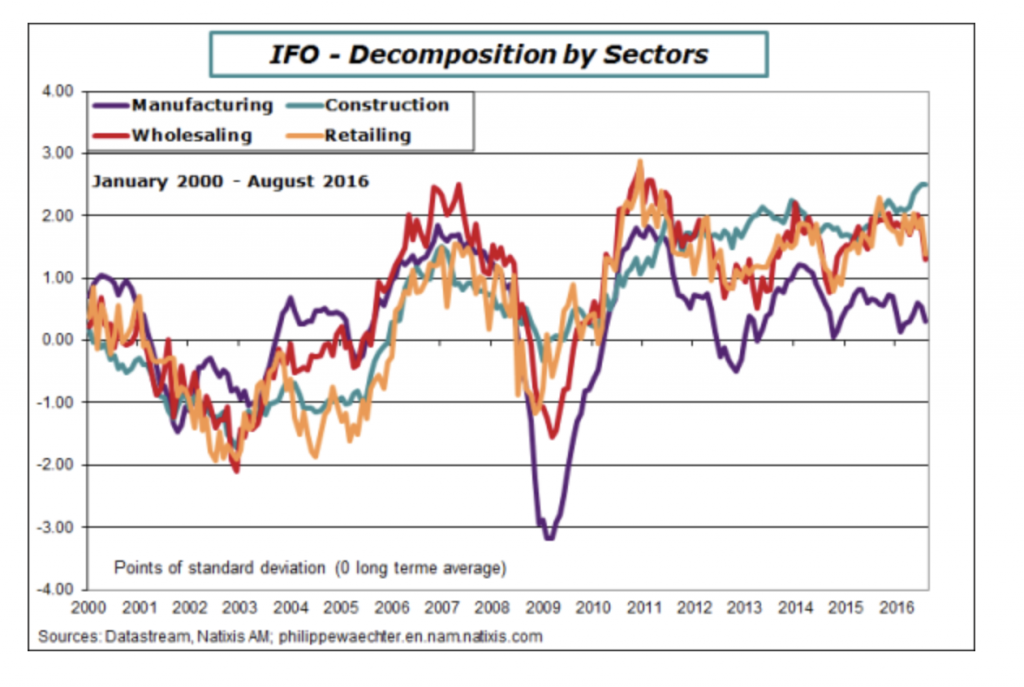

The detail of each survey shows that internal demand has been weaker in August.

This can be seen on the German graph below. There is a deep drop in retailing and in wholesaling in August.

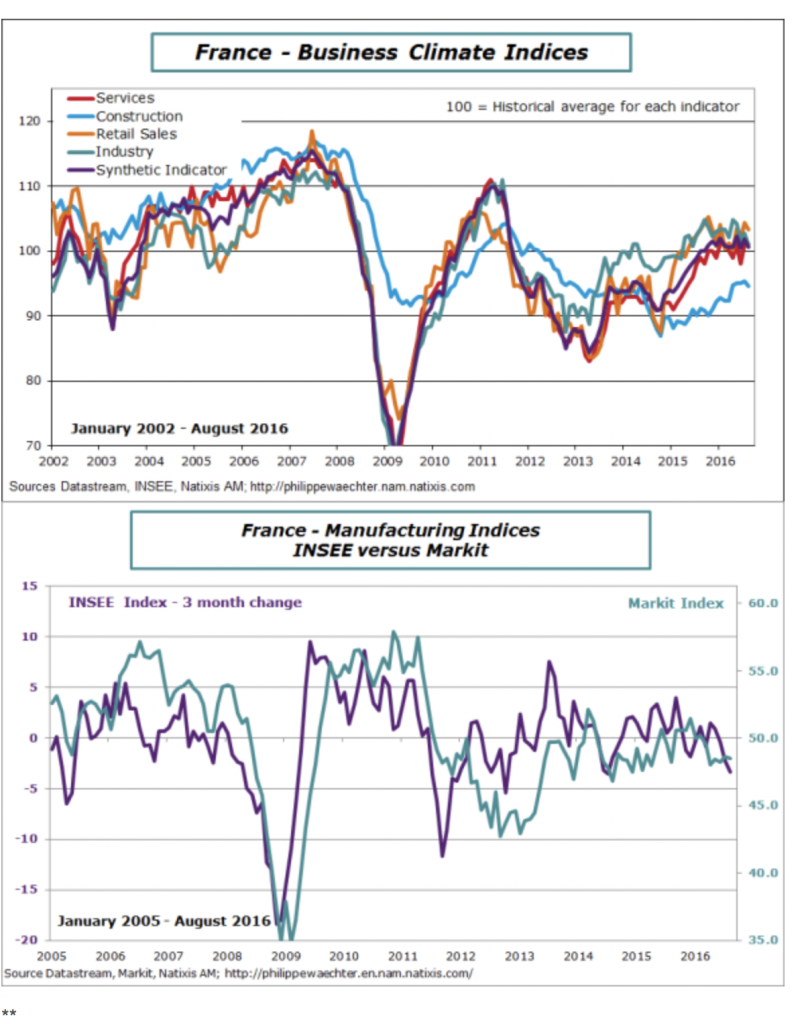

In France the main source of concern is the weaker momentum in the industry. All indices are close to their historical level (except construction) and there is no source of rapid improvement. The industrial sector was perceived as stronger 3 to 6 months ago but this is no longer the case and its recent momentum is problematic. This means that we can have a rebound in the third quarter for GDP (after 0 in Q2) but the government target growth of 1.5% for 2016 will not be reached.